State of the market – Autumn 2026

‘Resilience’ – it’s not just a word used to inspire athletes and children.

As we had into the cooler months of 2026, it’s also a term being applied liberally to the property market, which is proving its ongoing strength in the face of interest rate rises, fuel shortages, increased inflation, and uncertain world affairs.

So as the weather cools, and attention turns to the brief Easter break ahead, let’s take a quick spin through the data, looking at what’s been happening and what’s likely to occur in the property market for Autumn 2026.

Autumn trends

Autumn represents a bit of a sweet spot when it comes to Australia’s ever intriguing property market. After the rush of spring and lull of summer, this is a season where equilibrium tends to return.

In fact, Autumn is renowned as the second busiest selling season of the year, with March, April and May traditionally seeing an increase in listings, a rise in buyer inquiries and more auction competition.

But does the data support that this year? Let’s dive on in…

Home values

Australia’s housing values continue to sit at a record high, with the collective value of residential real estate now $12.5 Trillion, according to Cotality (formerly CoreLogic).

To put that into context, that equates to more than the stock market ($3.8 Trillion) and Australia’s collective superannuation ($4.5 Trillion) combined. In fact, an astounding 55.4 per cent of Australia’s wealth is currently in housing.

The current record high also respresents an increase of 9.9 per cent over the past 12 months. Cotality notes that represents the fastest 12-month pace of growth since June 2022.

“Every capital and rest of state region recorded an annual rise in values, ranging from 22 per cent in Perth to 4.7 per cent in Melbourne,” Cotality states.

That said, it’s not a one-speed market and that growth has slowed with February seeing values increase by just 0.8 per cent.

The mid-level capitals (Perth – 22 per cent increase, Darwin – 19.4 per cent increase and Brisbane – 17.3 per cent increase) outpaced the larger capitals of Sydney (6 per cent increase) and Melbourne (4.7 per cent increase) over the past 12 months while the combined regionals (11.1 per cent increase) outperformed the combined capitals (9.6 per cent increase)

Image: Cotality

Supply and demand

Cotality notes one of the key factors supporting growth in the housing markets is low supply.

Nationally, listing volumes remained 17.8 per cent lower than the five-year average, with 120,610 properties on the market in the four weeks ending March 1. That’s 14 per cent lower than the same time last year.

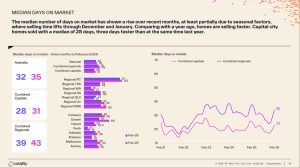

Days on market also remain low, averaging 32 days nationally, which means properties are selling three days faster than they did this time last year.

When is comes to the city versus the regionals, the combined cities average 28 days on market compared to 31 days last year, and the regionals are at 39, compared to 43 days on market this time last year.

Properties in Perth are the fastest to sell, averaging just 10 days on market.

Vendor discounting also remains low, with capital city sellers reducing their asking prices by a median of 2.9 per cent to reach the contract price, while regional sellers are discounting by a median of 3.2 per cent.

Rental market

While not seeing the steep gains of the pandemic, rental rates are continuing to increase.

Cotality notes nationally rents increased 5.5 per cent in the 12 months to February, with the combined capitals averaging 5.3 per cent, while regional areas saw average rent rises on 6 per cent.

Interest rates and world affairs

It would be remiss to talk about property prices and market conditions without also discussing the greater market forces and world affairs currently at play.

While we’re only three months into the year, we’ve already seen the Reserve Bank announce two cash rate increases of 0.25 per cent each to bring the current rate to 4.1 per cent.

At the March meeting the RBA board noted this was in a bid to tackle inflation, which picked up pace in the latter half of 2025.

World affairs, including the current war in the Middle East, are adding to this inflationary pressure, especially when it comes to increased fuel costs,

As for whether further cash rate increases will be needed, well that remains to be seen. But in the interim, it does have flow on effects into the housing market, particularly when it comes to borrowing power.

As PropTrack explains, for every increase of 0.50 percentage points in interest rates, the average person’s borrowing capacity falls by about 5 per cent.

The takeaway

Six years after the pandemic, Australia’s property market remains steadfast in its resilience even in the face of interest rate rise and unexpected world affairs.

There’s little indication this will change any time soon, with demand for properties continuing to outpace the available supply, particularly in the more affordable price brackets.

For those considering selling, it remains a positive market. For those considering buying, there are still opportunities available, but it’s critical to be proactive in your search and have your financial ducks in a row.