The State of the Market – Summer 2025

With the last of this year’s cash rate decisions now behind us and Christmas just around the corner, it’s a good time to reflect on how the property market has shaped up throughout 2025.

After all, it’s been another interesting year – one defined by continued property price rises, demand outpacing supply, and a welcome decrease in interest rates.

So let’s look back on 2025 while gazing into the crystal ball of what might be ahead in our State of the Market Report for Summer 2025.

What happens over summer?

Summer sees some interesting trends occur in the property market. There’s a rush on buying and selling in late spring and early summer, with vendors and purchasers all looking to finalise and settle things before the Christmas break.

This is evident in both listings data and also auction volumes which tend to peak in late November or early December before petering out in the immediate lead-up to Christmas.

The market then traditionally sees a quiet period until the end of January, when listings and sales start increasing in the lead-up to Easter.

Home values

Home values continued their upward trajectory throughout 2025, with October seeing values lift 1.1 per cent. Cotality noted this was the highest monthly gain since June 2023 and was likely driven by the three interest rate reductions delivered earlier in the year.

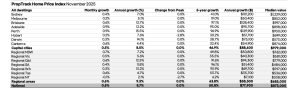

Meanwhile Proptrack notes National Home Prices are now at a record high, sitting at 8.7 per cent higher than they were a year ago.

Interestingly, their data indicates regional growth outpaced the capitals, with regional areas increasing by 9.3 per cent over the past 12 months, compared to 8.3 per cent for the major capitals.

In terms of median values, the national median house price is now $873,000. Breaking that down a little, the capital median value is $979,000, led by Sydney with a median value of $1,239,000, while the regional median value is $685,000.

Source: Proptrack

Supply and demand

Supply and demand continues to be one of the most interesting elements of the current property landscape.

While some sellers have been looking to capitalise on the higher property prices, supply is not keeping pace with demand.

Both Cotality and PropTrack note the expanded Home Guarantee initiative along with increased investor activity and population inflows are continuing to drive property demand, particularly in markets with a lower price point.

Meanwhile, the construction of new dwellings simply cannot keep up with the targets set by government.

“The imbalance between the supply and demand of housing has kept values on the rise even during periods of rate increases,” Cotality explains.

“This mismatch has persisted through 2025, where estimated sales in the three months to October (140,000), outpaced the 125,000 new listings observed by Cotality in the same period.

“While September building approvals data showed a strong increase, new housing construction continues to fall behind housing targets.”

Affordability is the big issue

By far the biggest issue affecting the property market in 2025 was affordability.

A recent report by Cotality noted Australia’s housing affordability was at an all-time low. This is illustrated by the fact it now takes on average 11 years to save a 20 per cent deposit for a property and 45 per cent of household income goes to servicing a new mortgage.

And this may have implications for housing prices down the track. PropTrack predicts that while there may be further price gains over the summer, “affordability constraints are likely to see price growth moderate throughout 2026”.

Source: Cotality

Auction insight

Auctions tend to act as a market litmus test, indicating everything from supply versus demand to general market confidence.

As we round out 2025, the combined capital city preliminary clearance rate for the week ending December 7 was 63.5 per cent. This was down on the week prior (68.2 per cent) but higher than the same time last year when it was 57.6 per cent.

In terms of volume, the number of properties heading to auction was trending higher than this time last year. In the first week of December last year, 2617 properties went under the hammer across the major capitals.

This year that increased to 3238, but Cotality notes the volume will now start to drop in the lead-up to Christmas.

“The number of auctions will cool further as we approach the festive season, with around 2880 homes scheduled for auction this week, before dropping sharply to around 1200 auctions over the week ending December 21,” Cotality said.

“Auction activity is likely to remain low until early February.”

Interest rates

On December 9, the Reserve Bank of Australia handed down its final cash rate decision of the year, opting to keep interest rates on hold at 3.6 per cent after delivering three cash rate cuts in 2025.

In February, they dropped rates by 25 basis points followed by a further 25 basis point cut in May then again in August.

Many predict the cash rate will now be on hold for the foreseeable future as the RBA seeks to rein in inflation, which ended the year higher than anticipated at 3.3 per cent.

And while the housing market isn’t the RBA’s actual focus when they consider whether to lower, raise or hold the cash rate, the two are inextricably linked.

Low interest rates tend to spur on borrowing, and as Cotality notes, “the pace of credit growth, the level of household debt and the wealth effects of housing can all shape economic outcomes”.

The takeaway

The past year has been another period of growth for the property market, particularly in affordable markets which are popular with first home buyers and investors.

As for what’s ahead, the market is likely to continue to remain strong, but growth looks set to be moderated by affordability constraints. It is also likely to be tempered by interest rates which are predicted to remain on hold while the RBA continues to tackle inflation.